How to Pay Off Debt Faster Without Destroying Your Lifestyle

This guide is based on research from nonprofit credit counseling organizations, consumer finance studies, and real-world debt payoff case analysis.

📘 In This Guide 👇

- Introduction to Concepts of Debt Payment

- Why Most People Stay in Debt

- Step-by-Step Plan to Pay Off Debt Faster and Build Financial Freedom

- Debt Snowball vs Debt Avalanche: Which Strategy Is Better?

- Tool #1: The Debt Crusher Calculator

- Tool #2: The Interest Rate Negotiation Script

- Real Example: From $18,000 in Debt to Zero in 22 Months

- Should You Use a Balance Transfer or Debt Consolidation Loan?

- How Long Does This Take?

- Final Thoughts: Debt freedom is not built through suffering

Introduction to Concepts of Debt Payment

It is a financial challenge that requires structure, clarity, and a deliberate plan — not exhaustion, fear, or endless self-denial.

Too many people attempt to escape debt by relying on extreme budgeting, rigid self-control, or temporary sacrifices they cannot sustain. While those methods may create short-term progress, they often lead to burnout, frustration, and relapse. The real problem is not a lack of discipline — it is the absence of a system designed for how people actually live, earn, and spend.

This guide is built on a more intelligent approach using smart budgeting systems . It combines financial mathematics, behavioral psychology, and practical money systems to help you eliminate debt efficiently without destroying your quality of life. Instead of forcing you to suffer your way to freedom, it shows you how to use strategy, structure, and smart decision-making to regain control of your finances — and keep it.

This guide is based on proven debt payment systems used by financial counselors, nonprofit credit agencies around the world.

These strategies align with consumer protection guidance from Consumer Financial Protection Bureau (CFPB) , and Federal Trade Commission (FTC) . The two organizations emphasize structured repayment planning, interest-rate negotiation, transparency in lending terms, and sustainable budgeting systems over extreme financial austerity.

Consumers are encouraged to verify APR structures, understand compounding interest mechanics, and explore hardship or retention programs before escalating financial stress.

Why Most People Stay in Debt

Most people remain in debt not because they lack discipline, but because they are operating inside broken financial systems that quietly keep them stuck.

- They do not have a clear, accurate picture of what they truly owe, making it impossible to plan effectively.

- They rely on credit to cover everyday expenses, which continuously replaces paid balances with new debt.

- They follow extreme budgeting methods that collapse under real-world pressure and lead to financial backsliding.

The objective of a smart debt strategy is not deprivation or stress. It is speed paired with sustainability — paying off debt as quickly as possible while maintaining a lifestyle you can realistically sustain.

You don’t need to give up your entire lifestyle — you need to eliminate waste and redirect power.

Step-by-Step Plan to Pay Off Debt Faster and Build Financial Freedom

This step-by-step plan shows you how to pay off debt faster using smart structure instead of extreme sacrifice. By following a clear, proven system, you reduce interest, accelerate progress, and regain control of your money while building a stable path toward long-term financial freedom.

1 — Find the Money You’re Already Wasting

Before trying to earn more money or forcing yourself into painful budgeting, start with the most powerful step: understanding where your money is actually going.

Review the last three months of your bank and card statements. If you need help organizing this process, start with our complete budgeting system guide. Go through each transaction and mark anything that meets one or more of the following conditions:

- You do not clearly remember making the purchase

- It did not meaningfully improve your life

- You would not miss it if it were removed

In most cases, these expenses fall into predictable categories such as forgotten subscriptions, impulse online purchases, unnecessary food deliveries, convenience fees, and underused apps or services. These are not essential costs — they are leakage points in your financial system.

This type of spending is known as grey-zone spending: money that provides neither real enjoyment nor long-term value. Eliminating it creates instant cash flow without reducing your quality of life.

Cut these expenses first. Keep what genuinely supports your health, relationships, and happiness — such as fitness, meaningful hobbies, and time with family. The goal is not to suffer. The goal is to redirect your money toward what truly matters and use the rest to win back your financial freedom.

Step 2 — Know Your True Debt Number

You cannot take control of a problem you cannot clearly see. Debt becomes overwhelming when it exists only as anxiety and uncertainty instead of precise, measurable numbers.

Begin by listing every debt you owe, including credit cards, personal loans, buy-now-pay-later plans, payday loans, and vehicle financing.

For each account, write down three critical details:

- The current balance

- The interest rate

- The required minimum payment.

This simple exercise transforms vague financial stress into concrete data. When your debt is organized and visible, it stops feeling chaotic and starts becoming manageable. Fear fades when replaced by facts — and facts give you the power to plan, prioritize, and take back control.

Step 3 — Choose the Right Payoff Strategy

There are two proven strategies for eliminating debt, and both work when applied consistently. The key is not choosing the “perfect” method — it is choosing the one you will actually follow through with.

Debt Snowball focuses on paying off your smallest balance first while making minimum payments on the rest. Each cleared account creates a quick psychological win, building confidence and motivation to keep going.

Debt Avalanche targets the debt with the highest interest rate first. This approach minimizes the total interest you pay and gets you out of debt at the lowest overall cost.

For many people, a hybrid method is the most effective. You eliminate one or two small, frustrating debts to create momentum, then shift your focus to the highest-interest balances with disciplined intensity.

The smartest plan on paper means nothing if you abandon it. The best strategy is the one that fits your behavior, keeps you engaged, and allows you to stay consistent until every balance is gone.

Tool #1: The Debt Crusher Calculator

Create this simple table in Excel or Google Sheets:

| Debt | Balance | APR | Minimum | Priority |

|---|---|---|---|---|

| Credit Card A | $4,500 | 22% | $90 | 1 |

Each month, interest is calculated as:

Interest = Balance × (APR ÷ 12)

Any amount you pay above the minimum goes directly to the principal — reducing future interest. This creates a compounding advantage in your favor.

Want to speed this up even more?

If you have high-interest credit cards, the fastest way to apply this system is by using a 0% balance transfer card or a low-interest debt consolidation loan. This lets you move expensive debt into a lower-interest account so more of your payment goes to the balance instead of interest.

See Your Best Debt OptionsStep 4 - Reduce Interest and Pay Off Debt Faster

High interest is the silent force that keeps many people trapped in debt. Even when you make consistent payments, a large portion of your money is often consumed by interest rather than reducing the actual balance.

This is why you should contact every lender and ask about available options such as:

- A lower annual percentage rate (APR)

- A temporary hardship rate

- A retention or loyalty offer

Many financial institutions are willing to reduce rates to keep customers from defaulting or transferring their balances elsewhere.

Even a small reduction of 3 to 5 percent can eliminate months of interest charges over time, allowing more of each payment to go toward the principal without increasing how much you pay. Lenders prefer to earn a little less rather than risk losing you completely — and using that leverage is one of the smartest ways to accelerate your debt payoff.

Tool #2: The Interest Rate Negotiation Script

Phase 1 — The Loyalty Ask

“Hi, my name is ___ and I’ve been a cardholder since ___. I’ve been reviewing my finances and noticed my APR is ___%. Since I have a strong history of on-time payments, I’d like to request a permanent reduction to something closer to 15%.”

Phase 2 — The Competitive Pressure (if they say no)

“I understand. However, I’ve received several 0% balance-transfer offers from other banks. I’d prefer to stay with you, but I can’t ignore the savings. Is there a retention offer or supervisor override available?”

Phase 3 — The Temporary Win (if they still resist)

“If a permanent reduction isn’t possible today, can we apply a temporary reduced rate for the next 6–12 months while I aggressively pay this down?”

Even a small rate drop can save thousands.

You can find more tools to reduce interest in our Loans & Debt resource hub.

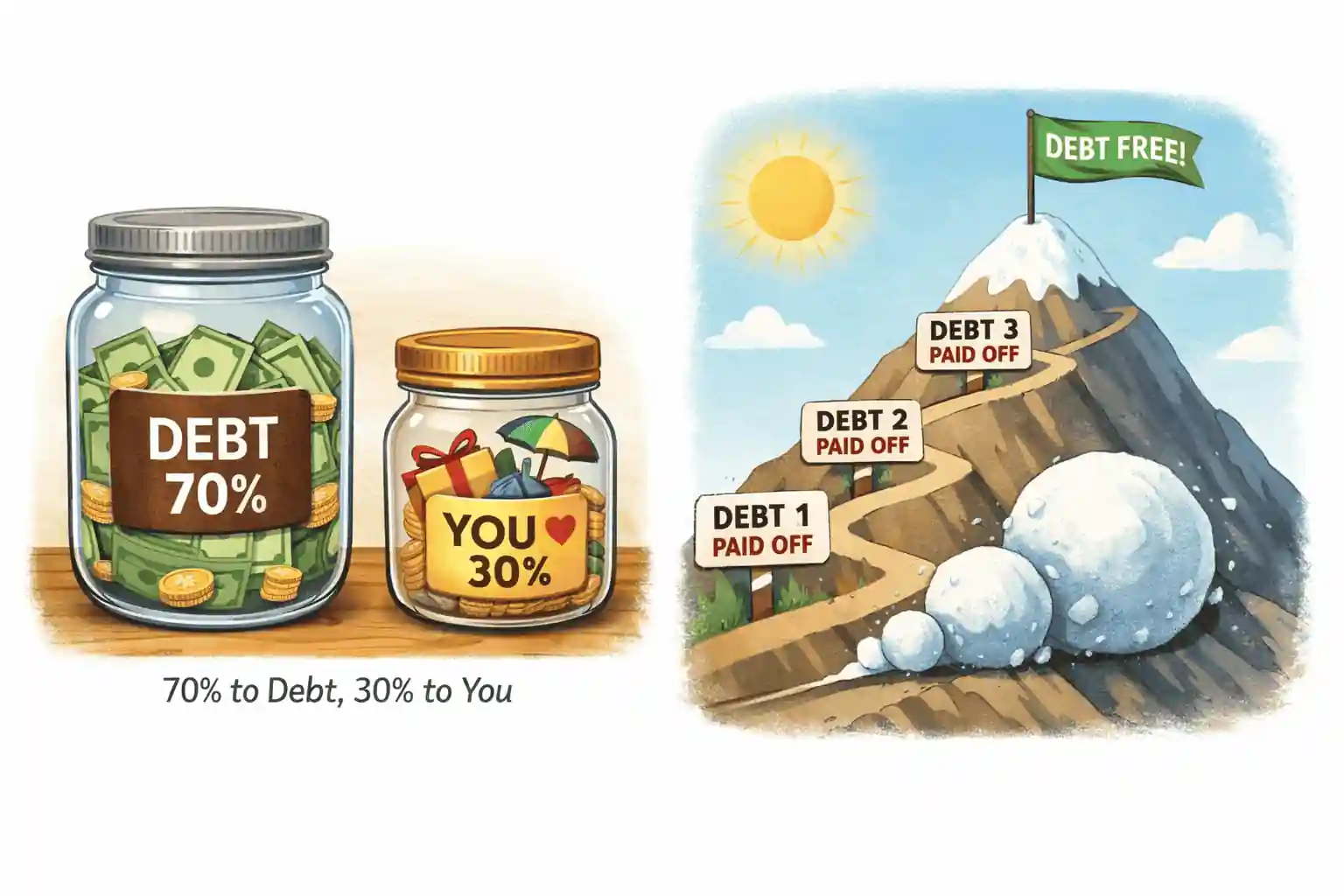

Step 5 — Use the Windfall Rule

Whenever you receive unexpected or extra income — such as a bonus, tax refund, cash gift, or side-hustle earnings — treat it as an opportunity to accelerate your debt payoff rather than absorb it into everyday spending. If you don’t yet have extra income, explore our beginner-friendly side hustle ideas.

A simple and effective rule is to divide that money into two parts: 70 percent goes directly toward debt, and 30 percent is set aside for you. The larger portion creates meaningful progress on your balances, while the smaller portion gives you permission to enjoy the reward without guilt.

This approach does more than improving your numbers — it rewires your mindset. Instead of viewing debt repayment as punishment, you begin to associate it with positive reinforcement. Over time, this makes consistency easier, motivation stronger, and long-term success far more likely.

Step 6 — Automate Your Attack

Willpower is unreliable, especially when money decisions have to be made every day. Strong financial results come from systems that work automatically in the background, not from constant self-control.

Set up your debt payments so they happen without requiring ongoing effort. Schedule automatic payments that are higher than the minimum, use bi-weekly payments where available to reduce interest faster, and activate round-up or spare-change features that send small extra amounts toward your balances.

When extra money is applied to your debt before you ever have a chance to spend it, your lifestyle stays largely unchanged — but your loan balances shrink much faster. Automation turns discipline into default behavior, which is exactly how lasting financial progress is built.

Step 7 — Track Your Debt Payoff and Stay Motivated

Progress becomes far more powerful when you can see it. Use a debt tracker, a simple spreadsheet, or even a visual progress bar to monitor your balances as they decline. Watching the numbers fall turns abstract effort into tangible achievement — and every reduction, no matter how small, is a real win.

When one debt is fully paid off, do not absorb that freed-up money into your spending. Instead, take the entire payment and apply it to the next debt on your list. This creates a compounding effect: each cleared balance increases the size of the next payment, accelerating your results and building unstoppable momentum. Over time, this “snowball” of payments turns small victories into rapid, powerful progress toward being debt-free.

Real Example: From $18,000 in Debt to Zero in 22 Months

Consider a real-world example of how structured repayment works when applied consistently.

A household carrying $18,000 in credit card debt at an average APR of 24% was making only minimum payments, barely reducing principal while interest accumulated each month.

Instead of resorting to extreme budgeting or eliminating all discretionary spending, they implemented a structured hybrid strategy:

- Eliminated two small balances first to create momentum (snowball effect)

- Negotiated their highest APR down from 24% to 17%

- Applied the 70/30 windfall rule to bonuses and tax refunds

- Automated bi-weekly payments above the minimum

- Redirected freed-up payments toward the highest-interest balance (avalanche phase)

Within 22 months, the entire $18,000 balance was eliminated — without extreme lifestyle sacrifice.

The difference was not income level or financial luck. It was structure, consistency, and interest optimization.

According to guidance from the National Foundation for Credit Counseling (NFCC) , structured repayment plans combined with interest negotiation consistently produce stronger long-term outcomes than unsustainable austerity strategies.

This example illustrates an important principle: debt freedom is rarely about intensity — it is about intelligent system design sustained over time.

Debt Snowball vs Debt Avalanche: Which Strategy Is Better?

Two dominant debt repayment strategies consistently outperform all others: the Debt Snowball and the Debt Avalanche. Both work — but they serve different psychological and financial needs.

Debt Snowball (Behavioral Momentum Method)

You focus on paying off the smallest balance first while making minimum payments on the rest. Once that debt is eliminated, its payment rolls into the next smallest balance.

Best for: People who need visible progress and motivational wins to stay consistent.

Debt Avalanche (Mathematical Efficiency Method)

You direct all extra payments toward the highest-interest debt first, minimizing total interest paid over time.

Best for: Individuals focused on minimizing long-term cost and accelerating payoff through interest optimization.

For many households, a hybrid approach works best: eliminate one or two small debts for momentum, then aggressively target the highest-interest accounts. The most effective strategy is not the one that looks best on paper — it is the one you can sustain consistently until every balance reaches zero.

Should You Use a Balance Transfer or Debt Consolidation Loan?

If your credit score qualifies, shifting high-interest credit card debt into a lower-interest structure can significantly accelerate payoff.

0% Balance Transfer Cards

These allow you to move existing credit card balances to a new card offering 0% introductory APR for a promotional period (typically 12–21 months). During this window, 100% of your payment reduces principal — not interest.

Best for: Individuals with strong credit and a clear repayment timeline.

Debt Consolidation Loans

A fixed-rate personal loan can combine multiple debts into one predictable monthly payment, often at a lower interest rate than revolving credit.

Best for: Those seeking structured repayment and simplified budgeting.

Before applying, compare fees, promotional terms, and total repayment cost. When used strategically, consolidation reduces interest drag and accelerates debt freedom. When used carelessly, it can extend repayment and increase total cost.

Explore structured borrowing options in our Loans & Debt resource hub.

How Long Does This Take?

When this system is applied consistently, many people are able to eliminate their debt within 12 to 36 months, depending on income level, debt size, and interest rates. However, the true measure of success is not how fast you finish — it is how well you are able to stay on track.

A plan only works if it is sustainable. What matters most is that you avoid burnout, maintain momentum, and do not fall back into old financial habits. By using a structured, realistic approach, you create steady forward progress that continues month after month until every balance is gone — and stays gone.

Learn More on SmartMoneyTrek

Explore our core financial guides:

- Save Money – proven ways to cut bills and build savings

- Budgeting – Tools and strategies to control your money

- Make Money – real side hustles and income ideas

- Loans & Debt – How to borrow wisely and eliminate debt

Frequently Asked Questions About Paying Off Debt

The fastest way to pay off credit card debt is to apply all extra payments toward the highest-interest balance while maintaining minimum payments on the others. This reduces total interest paid and accelerates overall payoff.

Build a small emergency fund covering one to three months of essential expenses before aggressively paying down debt. This prevents new borrowing when unexpected expenses occur.

Yes. Many credit card issuers offer hardship programs, promotional APR reductions, or retention offers if you request them directly — especially if you have a history of on-time payments.

Debt consolidation can be effective if it lowers your interest rate and shortens your repayment timeline. It is not beneficial if it significantly extends repayment or increases the total cost of the debt.

Any amount paid above the minimum reduces your principal immediately and lowers future interest charges. Even small but consistent additional payments can significantly accelerate debt payoff over time.

With consistent structured payments and interest optimization, many people eliminate consumer debt within 12 to 36 months. The timeline depends on income level, total debt size, and interest rates.

Final Thoughts: Debt freedom is not built through suffering

True debt freedom is not created through constant sacrifice or financial pain. It is built through smart systems, emotional stability, and mathematically sound strategies that work together to move you forward with confidence.

You do not need to ruin your lifestyle to eliminate your debt. With the right structure in place, you can make steady, powerful progress while still enjoying the things that make life meaningful.

Debt freedom becomes easier when paired with intentional saving strategies.

All it takes is a better plan — and now, you have one. 💛

This content is for educational purposes only and does not constitute financial advice.