Envelope Budgeting System: A Beginner’s Guide to Cash Budgeting

📘 In This Guide 👇

- Introduction Envelope Budgeting System

- What Is the Envelope Budgeting System?

- The Philosophy Behind Envelope Budgeting

- How to Set Up the Envelope Budgeting System

- Common Envelope Budget Categories

- Pros of the Envelope Budgeting System

- Cons of the Envelope Budgeting System

- Example of the Envelope Budgeting System in Practice

- The Modern Evolution: Digital Envelope Budgeting

- Who Should Use the Envelope Budgeting System?

- Tips for Making the System Successful

- Research Supporting Cash-Based Budgeting

- Frequently Asked Questions

- Final Thoughts

Introduction Envelope Budgeting System

Managing money successfully is rarely about how much you earn; it is about how well you control where your money goes. In a world dominated by digital payments, auto-subscriptions, and instant online purchases, spending has become almost invisible. As a result, many people find themselves wondering where their money disappeared before the end of the month.

One budgeting method has quietly stood the test of time despite these changes: the Envelope Budgeting System.

Though simple in design, this method is powerful because it introduces something modern finance often removes — intentional spending discipline. By assigning cash to specific spending categories and stopping once the money runs out, the envelope system creates natural financial boundaries that prevent overspending.

This guide explains how the envelope budgeting system works, its major advantages and disadvantages, and how modern users can adapt the system for today's digital economy.

If you're looking for a full budgeting system beyond percentage-based planning, read our complete monthly budgeting guide.

Envelope Budgeting System: Key Takeaways

- The envelope budgeting system divides income into spending categories using physical or digital envelopes.

- Each envelope has a fixed spending limit that cannot be exceeded.

- When the envelope is empty, spending stops until the next budgeting cycle.

- This method improves spending awareness and prevents impulse purchases.

- Digital versions now allow envelope budgeting without using physical cash.

This guide is based on proven budgeting systems used by financial counselors, nonprofit credit agencies, and long-term savers around the world.

At SmartMoneyTrek, we focus on practical personal finance systems designed for real people — especially those building stability from limited income.

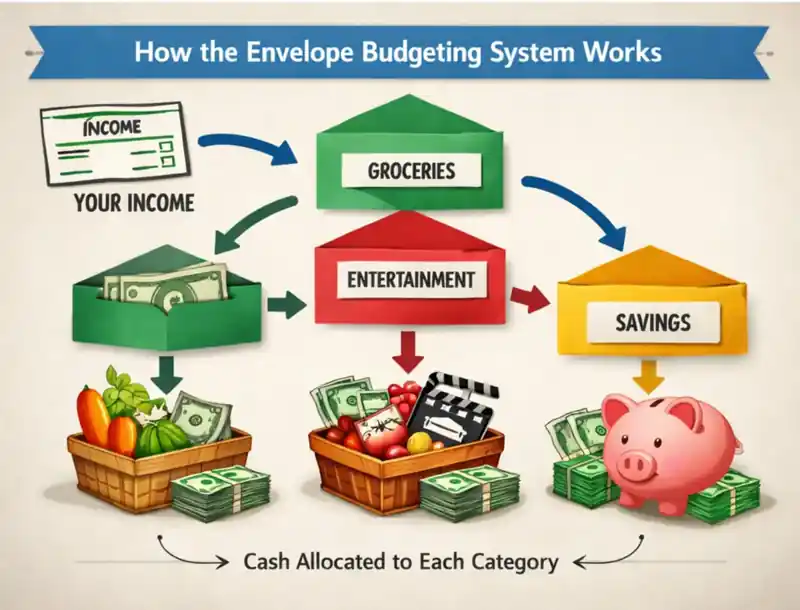

What Is the Envelope Budgeting System?

The envelope budgeting system is a money management method where income is divided into spending categories using envelopes. Each envelope contains a fixed amount of money for a specific expense such as groceries or entertainment. Once the money in the envelope runs out, spending in that category stops until the next budgeting period.

At the beginning of the budgeting period (usually monthly or bi-weekly), you allocate a fixed amount of money to each category. For example:

| Expense Category | Allocated Monthly Budget |

|---|---|

| Groceries | $300 |

| Transportation | $150 |

| Dining Out | $120 |

| Entertainment | $100 |

| Personal Care | $80 |

The allocated cash is placed into labeled envelopes. When spending occurs, the money must come from the relevant envelope.

The rule is simple but powerful: Once the envelope is empty, spending in that category stops until the next budgeting period. This rule creates a hard limit that protects your finances from impulsive purchases and uncontrolled spending.

Saving money works best when you are tracking every dollar with a monthly budget.

The Philosophy Behind Envelope Budgeting

Beyond its mechanical process, the envelope system works because it taps into powerful behavioral psychology. Digital payments make spending feel painless. Swiping a card or tapping a phone removes the emotional connection to money. Researchers often call this phenomenon the “pain of paying.”

When you use physical cash, that psychological friction returns.

You physically see the money leaving your hands.

You watch the envelope shrink.

You become more aware of every purchase.

This simple awareness encourages three essential financial behaviors:

- Intentional spending

- Accountability

- Prioritization of needs over wants

Instead of wondering where your income disappeared, you decide in advance where every dollar should go.

Not sure where to start? Our guide on how to build an emergency fund from scratch breaks it down step by step.

If you don’t yet have a simple tracking system, follow our complete beginner budgeting guide to see where your money is leaking and how to plug those holes.

How to Set Up the Envelope Budgeting System

1. Calculate Your Total Monthly Income

Begin by identifying your net monthly income—the amount you receive after taxes and deductions. Include all dependable income sources, such as salary or wages, side business revenue, freelance work, and passive income streams.

Having a clear and accurate view of your total income provides the financial foundation for a realistic budget, ensuring your spending limits align with what you truly earn.

2. Identify Your Spending Categories

Next, organize your expenses into clear spending categories. Pay particular attention to variable expenses, as these are the areas where overspending most commonly occurs.

Typical categories may include:

- Groceries

- Transportation or fuel

- Dining out

- Entertainment

- Personal care

- Household expenses

- Shopping or clothing

Keep your categories simple and focused, especially at the beginning. A streamlined structure makes the budgeting system easier to follow, maintain, and sustain over time.

3. Assign Spending Limits

Allocate a specific spending limit to each category based on your available monthly income. The combined total of all categories should never exceed your income, ensuring your budget remains balanced and sustainable.

Below is a simple example of how funds may be allocated:

| Category | Budget |

|---|---|

| Groceries | $300 |

| Transportation | $150 |

| Utilities | $200 |

| Dining Out | $120 |

| Entertainment | $100 |

| Miscellaneous | $80 |

The objective is to assign every dollar a clear purpose before spending begins, creating intentional control over how money is used.

4. Withdraw and Fill the Envelopes

Withdraw the allocated cash for each spending category and place the correct amount into clearly labeled envelopes.

Whenever you make a purchase, use money only from the corresponding envelope. This disciplined approach creates clear, visible spending limits and reinforces mindful spending.

By physically separating your money, the system introduces a natural control mechanism that helps prevent accidental overspending.

5. Track and Adjust

Budgeting is a dynamic process that improves with regular review. At the end of each month, evaluate your envelopes to identify which categories stayed within limits and which fell short.

For instance, if grocery funds run out early while entertainment money remains unused, adjust the allocations in the following month. Continuous review and refinement ensure your budget remains practical, balanced, and aligned with your real spending patterns.

If your income is currently limited, consider increasing it with realistic side income ideas for beginners.

Common Envelope Budget Categories

While every household budget is different, most people start with a few core spending categories when using the envelope budgeting system.

- Groceries

- Transportation and fuel

- Dining out

- Entertainment

- Personal care

- Household supplies

- Clothing and shopping

- Miscellaneous spending

These categories typically represent the most flexible expenses in a budget. Using envelopes for these areas helps prevent the gradual spending leaks that often derail monthly budgets.

Pros of the Envelope Budgeting System

Despite its traditional nature, the envelope budgeting method remains highly respected because of the powerful financial discipline it reinforces.

1. Strong Protection Against Overspending

One of the greatest strengths of envelope budgeting is its built-in spending limit. Once an envelope is empty, spending in that category stops.

Unlike digital payments that make overspending easy, this system removes the temptation to swipe a card or exceed your budget. As a result, it remains one of the most effective strategies for controlling everyday expenses and maintaining financial discipline.

2. Increased Spending Awareness

Using physical cash encourages greater mindfulness with every purchase. Each transaction requires you to consciously remove money from the envelope, making spending more tangible and deliberate.

As you see the remaining cash decline, you gain a clearer understanding of how quickly expenses accumulate. Over time, this heightened awareness fosters more thoughtful spending habits and stronger financial discipline.

3. Simple and Easy to Understand

The envelope system stands out for its simplicity and accessibility. Unlike complex spreadsheets or financial software, it relies on a clear and intuitive structure.

No technical knowledge or accounting expertise is required—the rules are straightforward, making the system easy for anyone to adopt and maintain.

4. Encourages Financial Discipline

Envelope budgeting cultivates essential long-term money habits, including:

- Planning spending in advance

- Prioritizing essential expenses

- Avoiding impulse purchases

Over time, these practices strengthen self-control and build the core discipline required for effective and sustainable financial management.

5. Useful for Eliminating Debt

The envelope system can be especially effective for individuals working to eliminate debt. By restricting spending to available cash, it removes the ability to rely on credit cards or additional borrowing.

This cash-based approach promotes stricter spending control and helps individuals regain financial stability while steadily reducing outstanding debt.

If you’re starting from zero, read our step-by-step emergency fund guide to build financial security faster.

Cons of the Envelope Budgeting System

While the envelope budgeting method is highly effective for controlling spending, it also comes with certain limitations in today’s increasingly digital financial environment.

Understanding these challenges helps you determine whether the system aligns with your lifestyle and financial habits.

1. Inconvenient in a Digital Economy

One of the main challenges of the envelope system is its limited compatibility with today’s digital economy. Many everyday transactions now occur online, including utility bills, streaming subscriptions, online shopping, and other digital services.

Because these payments cannot be made with physical cash, managing them within a traditional envelope system can become inconvenient and less practical.

2. Security Risks of Carrying Cash

Relying heavily on physical cash can expose you to certain security risks, including theft, loss, or misplacement.

Unlike funds stored in bank accounts or protected by credit cards, lost cash cannot be traced or recovered, making this a notable drawback of the envelope budgeting system.

3. No Rewards or Cashback Benefits

Another limitation of the envelope system is the absence of credit card benefits. Many credit cards provide rewards such as cashback, travel points, and purchase protection.

Relying solely on cash means forgoing these incentives, which can otherwise add meaningful value to everyday spending.

4. Requires Consistent Discipline

The envelope system delivers results only when its rules are followed consistently. If you frequently borrow from other envelopes or switch to credit cards once cash runs out, the structure quickly breaks down.

Maintaining strict adherence is essential for the system to preserve its spending limits and financial control.

5. Limited for Complex Financial Planning

Envelope budgeting is highly effective for managing daily spending, but it is not designed to handle broader financial strategies such as investing, retirement planning, or long-term wealth building.

To achieve these larger financial goals, the system must be complemented with additional financial planning tools and strategies.

For those who prefer more precision and control, zero-based budgeting assigns every dollar a specific purpose.

Example of the Envelope Budgeting System in Practice

Imagine a household with a monthly take-home income of $3,000. After covering fixed expenses such as rent, insurance, and utilities, $900 remains for flexible spending categories.

Instead of leaving this money in a checking account, the envelope system divides it into controlled spending limits:

- $350 for groceries

- $150 for transportation

- $150 for dining out

- $100 for entertainment

- $150 for miscellaneous expenses

Each purchase must come from its corresponding envelope. If the dining envelope runs out after three weeks, dining out stops until the next month.

This simple rule forces spending awareness and prevents small purchases from gradually draining the budget.

High monthly bills often lead to debt. If that’s your situation, visit our how to reduce debt and stop high interest payments eating your income.

The Modern Evolution: Digital Envelope Budgeting

As financial transactions increasingly move online, many people now adopt digital versions of envelope budgeting. These systems replicate the traditional concept through budgeting apps or banking platforms, where money is assigned to virtual spending categories instead of physical envelopes.

Digital envelope budgeting offers several advantages:

- Easier bill payments

- Automatic expense tracking

- No need to carry physical cash

- Seamless compatibility with online purchases

Despite the technological shift, the core principle remains the same: always verify the available balance in a category before making a purchase.

If your income is tight, learn realistic ways to increase your income so you can improve your savings rate.

Who Should Use the Envelope Budgeting System?

The envelope budgeting method is particularly effective for individuals who:

- Struggle with overspending

- Prefer a simple and structured budgeting approach

- Want clear and firm spending limits

- Are working to eliminate debt

- Need stronger financial discipline

It also serves as an excellent starting point for beginners seeking to build practical money management habits and gain greater control over their finances.

Tips for Making the System Successful

To maximize the effectiveness of envelope budgeting, apply a few practical strategies that keep the system simple and sustainable.

1. Start with a Few Categories

Avoid creating too many envelopes at the beginning. A complex structure can quickly become difficult to manage. Instead, start with your major spending categories—such as groceries, transportation, and entertainment—and expand gradually as you become more comfortable with the system.

2. Maintain a Small Emergency Envelope

Unexpected expenses are inevitable. Setting aside a small emergency envelope provides a financial buffer for minor surprises.

This safeguard helps prevent unplanned costs from disrupting your overall budget and forcing adjustments to essential spending categories.

3. Review Your Budget Regularly

Spending patterns naturally evolve over time. Reviewing your envelopes at the end of each month allows you to identify necessary adjustments.

Regular evaluation ensures your budget remains realistic, responsive, and aligned with your current financial needs.

4. Combine Budgeting With Savings Goals

Budgeting should go beyond controlling expenses—it should also support long-term financial growth.

Make it a priority to allocate a portion of your income toward savings, investments, and future financial goals, ensuring your budget contributes to building lasting financial security.

Research Supporting Cash-Based Budgeting

Financial counselors and behavioral economists have long observed that cash-based budgeting methods can reduce impulsive spending and improve financial awareness.

Research published by the Consumer Financial Protection Bureau (CFPB) highlights how many households struggle to track everyday spending, which is why simple budgeting systems that create clear spending limits can improve money management habits.

Behavioral economics also explains the concept known as the “pain of paying.” Studies have found that people tend to spend less when using cash because physically handing over money increases awareness of the cost of each purchase.

Cash-based budgeting systems such as the envelope method take advantage of this psychological effect by creating visible spending boundaries. If you want to see how this system fits into a full financial plan, read our complete guide to creating a monthly budget.

Learn More on SmartMoneyTrek

Explore our core financial guides:

- Save Money – proven ways to cut bills and build savings

- Budgeting – Tools and strategies to control your money

- Make Money – real side hustles and income ideas

- Loans & Debt – How to borrow wisely and eliminate debt

Frequently Asked Questions

Yes. The envelope budgeting system is highly effective for controlling spending because it creates clear financial limits. Once the money in an envelope is gone, spending in that category stops, which helps prevent overspending and encourages better money discipline.

Yes. Many people now use digital envelope budgeting tools that allow them to assign money to spending categories electronically while maintaining the same budgeting principles.

Envelope budgeting works best for variable expenses such as groceries, dining out, transportation, entertainment, and shopping. These categories are easier to control when spending limits are clearly defined.

Beginners should start with three to five main envelopes to keep the system simple and manageable. More categories can be added later as budgeting habits improve.

Final Thoughts

The Envelope Budgeting System remains one of the most practical and time-tested methods for managing personal finances.

Its power lies in its simplicity. By assigning every dollar a purpose and limiting spending to the money available, the system introduces discipline, clarity, and control into everyday financial decisions.

While it may feel traditional in an increasingly digital world, the underlying philosophy is timeless: plan your spending before your money disappears.

Whether you use physical envelopes or digital budgeting tools, the envelope system can transform your relationship with money and help you build a stronger financial future.

Ready to Apply This Budgeting Method?

Learn how to create a simple monthly budget step by step and start organizing your income today. Create Your Monthly Budget.

Your financial journey doesn’t need to begin with perfection. It simply needs to begin with consistency — because consistent action, over time, is what turns small steps into lasting progress.

This content is for educational purposes only and does not constitute financial advice.