How to Create a Zero-Based Budget: The Complete Beginner’s Guide to Total Money Control

📘 In This Guide 👇

- Introduction to Zero-Based Budget

- Who Popularized Zero-Based Budgeting?

- What Is Zero-Based Budgeting?

- Why Zero-Based Budgeting Works (When Other Budgets Fail)

- The Core Advantages of Zero-Based Budgeting

- How Zero-Based Budgeting Compares to Traditional Budgeting

- Zero-Based Budgeting: Business vs. Personal Finance

- Step-by-Step: How to Create a Zero-Based Budget

- Real-Life Budget Example (Single Person)

- Real-Life Budget Example (Family of Four)

- The Psychology Behind Zero-Based Budgeting

- Common Beginner Mistakes (And How to Avoid Them)

- Zero-Based Budgeting for Irregular Income

- Zero-Based Budgeting vs The 50/30/20 Rule

- Pros and Cons of Zero-Based Budgeting

- Is Zero-Based Budgeting Realistic?

- Is Zero-Based Budgeting Stressful?

- How Long Should You Try Zero-Based Budgeting?

- Can Couples Use Zero-Based Budgeting?

- Zero-Based Budgeting for Low Income Earners

- Zero-Based Budgeting vs the Envelope System

- Best Tools for Zero-Based Budgeting

- How Often Should You Review Your Budget?

- Can Zero-Based Budgeting Help You Save More?

- Frequently Asked Questions

- The Long-Term Impact of Zero-Based Budgeting

- Final Thoughts: Becoming the CEO of Your Money

Introduction to Zero-Based Budget

Money rarely vanishes in one dramatic moment. More often, it slips away quietly — through forgotten subscriptions, small impulse purchases, and subtle lifestyle upgrades that seem harmless at the time but accumulate over months. Then one day you check your account balance and wonder:

“Where did it all go?”

If that feeling is familiar, the issue likely isn’t a lack of discipline. It’s a lack of structure. That’s where zero-based budgeting comes in.

Zero-based budgeting provides a clear, intentional framework for managing your income. Instead of letting money drift toward expenses, it assigns every dollar a specific purpose before the month begins. The result is clarity, control, and confidence in your financial decisions.

In this guide, you’ll learn:

- What zero-based budgeting actually means

- How the system works in practice

- Why it’s so effective for eliminating waste and increasing savings

- How to set it up from scratch

- The common beginner mistakes to avoid

By the end, you won’t just understand zero-based budgeting — you’ll know exactly how to implement it effectively and make it work for you.

If you're new to budgeting or want a complete framework, start with our complete guide to creating a monthly budget that actually works. This article focuses specifically on the zero-based budgeting method.

This guide is based on proven budgeting systems used by financial counselors, nonprofit credit agencies, and long-term savers around the world.

At SmartMoneyTrek, we focus on practical personal finance systems designed for real people — especially those building stability from limited income.

Who Popularized Zero-Based Budgeting?

Zero-based budgeting gained mainstream recognition through financial educators such as Dave Ramsey , who popularized the concept of giving every dollar a specific purpose within a monthly plan. The method was later integrated into digital budgeting platforms like You Need A Budget (YNAB) , which operationalizes the philosophy by encouraging users to proactively assign every dollar a defined role before spending.

What Is Zero-Based Budgeting?

Zero-based budgeting (ZBB) is a structured approach to money management in which every dollar of income is assigned a specific purpose before the month begins.

The core principle is straightforward: Income – Expenses – Savings – Debt Payments = $0

Reaching zero does not mean spending all your money. It means giving every dollar a clear role — whether that role is paying bills, building savings, investing, or reducing debt. Nothing is left unplanned or unaccounted for.

For example, if you earn $3,000 this month, you would allocate the full $3,000 across categories such as:

- Rent or mortgage

- Utilities

- Groceries

- Transportation

- Insurance

- Savings

- Investments

- Debt repayment

- Personal spending

By the time you complete your budget, every dollar has been assigned. There are no “extra” funds floating around without direction. That’s the essence of zero-based budgeting.

It isn’t about limiting yourself or creating financial pressure. It’s about making deliberate decisions with your money so it aligns with your priorities.

Saving money works best when you are tracking every dollar with a monthly budget.

Why Zero-Based Budgeting Works (When Other Budgets Fail)

Most traditional budgets are reactive. They follow a familiar pattern:

- Estimate your expenses.

- Try to stay within limits.

- Hope there’s money left over.

The weakness? There’s no clear assignment for every dollar, so unplanned money often gets spent without intention.

Zero-based budgeting changes the question entirely. Instead of asking, “What’s left?” You ask, “Where should this go?”. That shift is powerful.

It moves you from passive tracking to proactive planning. Every dollar is directed before it’s spent, which reduces waste, strengthens discipline, and gives you full control over your financial priorities.

If you don’t yet have a simple tracking system, follow our complete beginner budgeting guide to see where your money is leaking and how to plug those holes.

The Core Advantages of Zero-Based Budgeting

1. Complete Visibility

Every dollar is accounted for, giving you a clear and accurate view of where your money goes.

2. Intentional Decision-Making

Spending becomes a conscious choice, not an emotional reaction or impulse.

3. Faster Debt Repayment

Surplus funds are assigned strategically to debt, accelerating payoff instead of disappearing into unplanned expenses.

4. Stronger Savings Habit

Savings is built into the plan from the start, treated as a priority rather than an afterthought.

5. Immediate Leak Detection

Overspending stands out quickly, allowing you to adjust before small issues become larger problems.

Zero-based budgeting doesn’t just organize your finances — it strengthens your financial discipline and sharpens your decision-making.

How Zero-Based Budgeting Compares to Traditional Budgeting

Zero-Based Budgeting vs Traditional Budgeting

| Feature | Traditional Budget | Zero-Based Budget |

|---|---|---|

| Starting Point | Based on previous month’s spending | Starts from a clean slate each month |

| Planning Style | Estimate expenses and adjust as needed | Assign every dollar a specific role in advance |

| Savings Approach | Save whatever remains at month-end | Allocate savings intentionally from the start |

| Overspending Detection | Often goes unnoticed until late | Becomes immediately visible |

| Level of Control | Moderate | Maximum and proactive |

Traditional budgets adjust the past.

Zero-based budgeting intentionally designs the future.

Zero-Based Budgeting: Business vs. Personal Finance

| Aspect | Corporate Zero-Based Budgeting | Personal Zero-Based Budgeting |

|---|---|---|

| Primary Purpose | Improve cost efficiency and align spending with strategic business objectives. | Gain control over income, expenses, and financial goals. |

| Starting Point | Each department builds its budget from zero every cycle. | Every dollar of income is assigned a specific role before the month begins. |

| Decision Criteria | Expenses must be justified based on value contribution and expected return. | Expenses must support necessities, priorities, or long-term goals. |

| Scope | Organization-wide across departments, projects, and cost centers. | Individual or household income and expense categories. |

| Outcome Focus | Profitability, operational efficiency, and resource optimization. | Cash flow control, debt reduction, and savings growth. |

While corporate zero-based budgeting functions as a strategic cost-management framework for organizations, its personal finance adaptation focuses on intentional money management and disciplined spending. Both models operate on the same core principle—justifying every expense from a zero base—but differ in scale, complexity, and objectives. Addressing both perspectives strengthens topical authority and expands keyword relevance across business and personal finance search intent.

Step-by-Step: How to Create a Zero-Based Budget

Let’s turn this into a clear, practical execution plans:

1: Calculate Your Total Monthly Income

Start by determining the exact amount of money you can realistically allocate for the month. Include all reliable income sources:

- Salary (after tax)

- Side hustle income

- Freelance earnings

- Rental income

- Any consistent monthly cash flow

If your income fluctuates, use your lowest average month as your planning baseline. This creates a buffer and prevents overcommitting your money.

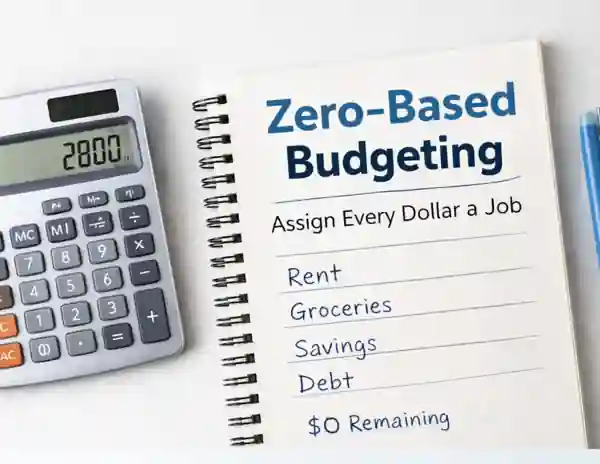

Example:

Monthly take-home pay: $2,800

That $2,800 becomes your total allocation pool — every dollar must be assigned a purpose.

2: Identify Your Fixed Expenses

Next, outline your fixed monthly obligations — the expenses that remain consistent and are typically non-negotiable. These often include:

- Rent or mortgage

- Insurance premiums

- Loan repayments

- Subscriptions

- School fees

- Internet services

Because these costs are predictable, they form the foundation of your budget and must be covered first.

Example:

- Rent: $1,000

- Insurance: $150

- Car payment: $250

- Internet: $60

Total Fixed Expenses is $1,460. This amount represents your baseline commitment each month before allocating funds to variable expenses, savings, or discretionary spending.

3: Estimate Your Variable Expenses

Variable expenses are costs that change from month to month. While they’re less predictable than fixed bills, they still require intentional planning. Common examples include:

- Groceries

- Gas or transportation

- Utilities

- Dining out

- Entertainment

- Personal care

To estimate accurately, review your last 2–3 months of bank statements. This helps you base your numbers on real spending patterns, not guesswork. Example:

- Groceries: $400

- Gas: $150

- Utilities: $120

- Eating out: $100

- Personal spending: $150

Total Variable Expenses is $920. This figure represents your flexible spending zone — the area where adjustments can significantly improve your financial control.

4: Allocate Savings and Debt Payments

This is where zero-based budgeting truly sets itself apart. Rather than saving whatever remains at the end of the month, you assign savings and debt payments intentionally — just like any other expense.

Common allocation categories include:

- Emergency fund

- Retirement contributions

- Investments

- Additional loan payments

By planning these upfront, you ensure financial progress is built into your budget — not dependent on leftover money. Example:

- Emergency fund: $200

- Extra debt payment: $220

In zero-based budgeting, savings and debt reduction are priorities, not afterthoughts.

5: Make Your Budget Equal Zero

Now bring everything together and ensure your allocations match your total income.

- Income: $2,800

- Fixed Expenses: $1,460

- Variable Expenses: $920

- Savings & Debt Payments: $420

- Total Allocated: $2,800

- Remaining Balance: $0

When your balance reaches zero, it means every dollar has been assigned a clear purpose. Nothing is unplanned. Nothing is drifting. At this point, you’ve successfully created your first zero-based budget — a structured plan where your money works with intention from the very beginning of the month.

High monthly bills often lead to debt. If that’s your situation, visit our how to reduce debt and stop high interest payments eating your income.

Real-Life Budget Example (Single Person)

Monthly Income: $2,000

Here’s how a zero-based budget might be structured:

- Rent: $800

- Utilities: $120

- Groceries: $300

- Transportation: $150

- Insurance: $100

- Phone: $60

- Personal spending: $100

- Emergency savings: $150

- Debt repayment: $220

Total Allocated: $2,000

Unassigned Balance: $0

Every dollar is given a defined purpose — covering essentials, allowing personal flexibility, building savings, and reducing debt.

Clear ➡️ Controlled ➡️ Intentional

If your income is tight, learn realistic ways to increase your income so you can improve your savings rate.

Real-Life Budget Example (Family of Four)

Monthly Income: $4,500

A zero-based budget for a family might look like this:

- Mortgage: $1,500

- Utilities: $300

- Groceries: $800

- Transportation: $400

- Insurance: $350

- School & children’s expenses: $300

- Entertainment: $200

- Emergency savings: $300

- Investments: $200

- Extra debt payment: $150

Total Allocated: $4,500

Unassigned Balance: $0

Every dollar is intentionally directed — covering household needs, supporting the children, building savings, investing for the future, and reducing debt. Nothing is left to chance.

The Psychology Behind Zero-Based Budgeting

Zero-based budgeting works because it removes frictional spending — the small, unconscious purchases that quietly drain your income over time.

When every dollar has a defined role:

- Impulse purchases require a conscious trade-off.

- Spending decisions are measured against your priorities.

- Short-term desires are weighed against long-term goals.

This structure changes more than your numbers — it changes your mindset.

You stop reacting to money and start directing it. You move from being a spender to becoming a planner. And when your identity shifts, your behavior naturally follows.

Common Beginner Mistakes (And How to Avoid Them)

1. Overlooking Irregular Expenses

Many beginners budget only for monthly bills and forget non-monthly costs such as car repairs, birthdays, holiday spending, or annual subscriptions. When these expenses appear, they feel unexpected — and disrupt the budget.

Solution: Use sinking funds.

A sinking fund allows you to set aside small amounts each month for future expenses. For example, if your car insurance costs $600 per year, divide it by 12 and budget $50 per month. By the time the bill is due, the money is already prepared. Planning for irregular expenses keeps your zero-based budget stable and prevents financial surprises from becoming setbacks.

2. Being Too Restrictive

Cutting groceries or entertainment too aggressively may look disciplined on paper, but it often leads to frustration and budget fatigue. When a plan feels unrealistic, it becomes difficult to sustain.

Solution: Build in realistic flexibility.

Allow reasonable amounts for enjoyment and everyday living. A sustainable budget balances discipline with practicality — it should support your life, not punish it.

3. Relying on a Large “Miscellaneous” Category

A broad miscellaneous category often becomes a catch-all for untracked spending. When too much money flows into a vague label, it hides patterns and reduces accountability.

Solution: Be specific. Clarity creates control.

Break expenses into clear, defined categories. The more precise your budget, the easier it is to identify waste, adjust intentionally, and stay in control of your finances.

4. Failing to Track Spending

Creating a budget without monitoring your actual spending turns it into a theoretical plan rather than a practical system. Without tracking, small deviations compound and the numbers quickly lose accuracy.

Solution: Review weekly.

Set aside time each week to compare your spending against your budget. Regular check-ins keep your plan aligned with reality and allow you to make adjustments before small gaps become major setbacks.

5. Ignoring a Cash Buffer

Even if your budget balances to zero, running your checking account too tightly can create unnecessary stress. Small timing differences — such as delayed deposits or early bill withdrawals — can trigger overdrafts.

Solution: Maintain a modest buffer.

Keep a cushion of $100–$200 in your checking account. It won’t disrupt your zero-based plan, but it will protect you from fees, surprises, and cash-flow timing issues.

Zero-Based Budgeting for Irregular Income

Freelancers, commission earners, and business owners can successfully use zero-based budgeting — it simply requires a more conservative foundation.

Use this approach:

- Budget based on your lowest expected monthly income. This prevents overcommitting during slower months.

- Cover essentials first. Prioritize housing, utilities, food, insurance, and minimum debt payments.

- Direct surplus strategically. In higher-income months, allocate extra funds to savings, debt reduction, or an income buffer.

- Build a 1–3 month reserve. An income cushion stabilizes cash flow and reduces financial stress.

Zero-based budgeting remains effective with irregular income — it just demands intentional planning and disciplined flexibility.

Zero-Based Budgeting vs The 50/30/20 Rule

The 50/30/20 rule allocates income into broad percentages:

- 50% for needs

- 30% for wants

- 20% for savings

It’s simple and easy to apply, making it useful for beginners who want a quick framework. Zero-based budgeting, however, goes deeper.

It provides:

- Greater customization for your exact financial situation

- Detailed control over every dollar

- Faster debt repayment through intentional allocation

- Clear visibility that exposes spending leaks quickly

If you prefer simplicity, the 50/30/20 rule works. If you want precision, structure, and accelerated progress, zero-based budgeting offers a stronger advantage.

Pros and Cons of Zero-Based Budgeting

Pros

- Provides maximum financial clarity

- Encourages deliberate, values-based spending

- Accelerates debt repayment through focused allocation

- Builds consistent savings discipline

- Adapts to any income level

Cons

- Requires more time to set up initially

- Demands consistent monthly review

- May feel restrictive during the adjustment phase

The first month requires focused effort and honest evaluation. Once the structure is in place, maintaining the system becomes far simpler — and far more rewarding.

Is Zero-Based Budgeting Realistic?

Yes — but realism depends on how you structure it. Zero-based budgeting is realistic when categories reflect your actual lifestyle rather than idealized spending targets. If you underestimate groceries, transportation, or personal expenses, the system can feel restrictive. However, when based on real spending data from previous months, zero-based budgeting becomes highly practical and sustainable.

The key is flexibility. The budget must still equal zero, but you can adjust category allocations as needed. Realistic planning creates long-term success.

Is Zero-Based Budgeting Stressful?

For some beginners, the first month can feel mentally demanding because every dollar must be assigned. However, that structure quickly reduces long-term stress. Financial anxiety often comes from uncertainty. Zero-based budgeting replaces uncertainty with clarity.

Once the system becomes routine, most people report feeling more in control — not more pressured.

How Long Should You Try Zero-Based Budgeting?

Commit to at least three months. The first month reveals spending habits. The second month improves accuracy. By the third month, the structure begins to feel natural.

Like any system, zero-based budgeting improves with iteration. Short-term experimentation is not enough to measure its effectiveness.

Can Couples Use Zero-Based Budgeting?

Yes — and it can be especially effective for couples. A shared zero-based budget encourages communication, transparency, and aligned financial priorities. Both partners agree in advance how income will be allocated.

Some couples choose joint budgeting with individual discretionary categories. This allows structure while maintaining personal autonomy.

Zero-Based Budgeting for Low Income Earners

Zero-based budgeting is particularly powerful for low income households because it eliminates unplanned spending. When income is limited, every dollar must work efficiently.

By prioritizing essentials first and assigning even small amounts toward savings or debt reduction, low income earners can build stability gradually. The system creates clarity — even when income is tight.

Zero-Based Budgeting vs the Envelope System

Both systems aim to control spending, but they operate differently. The envelope system uses physical cash divided into labeled envelopes for each spending category. Once an envelope is empty, spending stops.

Zero-based budgeting can include the envelope method, but it is broader. It assigns every dollar a job across all categories — including digital payments, savings, and debt. The envelope system is a tactical tool. Zero-based budgeting is a complete financial framework.

If you prefer a more flexible structure, consider the 50/30/20 budgeting rule, which divides income into fixed percentage categories instead of assigning every dollar a job.

Best Tools for Zero-Based Budgeting

You don’t need complex software to make zero-based budgeting work. The system is simple — the key is consistent use.

Practical options include:

- A basic spreadsheet

- Printable budget templates

- Budgeting apps

- Manual tracking in a notebook

- The envelope cash system

Each tool can be effective if used consistently. Success in zero-based budgeting doesn’t depend on the platform you choose — it depends on your commitment to reviewing, adjusting, and following the plan each month.

How Often Should You Review Your Budget?

At a minimum, review your budget at three key points:

- Before the month begins: Create and finalize your allocation plan.

- Mid-month: Check your progress and adjust if necessary.

- End of the month: Evaluate what worked, identify gaps, and refine for next month.

Budgeting is not a one-time setup. It’s an ongoing monthly discipline that keeps your finances aligned with your goals.

Can Zero-Based Budgeting Help You Save More?

Yes — significantly. Unassigned money tends to get spent without intention. Assigned money moves toward a purpose.

Zero-based budgeting makes savings a planned priority, not something you attempt with whatever remains. By giving savings its own category from the start, you create consistency and momentum. When saving is intentional, financial security doesn’t happen by chance — it accelerates by design.

Frequently Asked Questions

Yes. It builds financial awareness quickly by assigning every dollar a purpose, creating structure and control from the start.

No. Entertainment and personal spending are included — they are simply planned intentionally within clear limits.

You adjust by moving money from another category. The total allocation must still equal your total income.

Your first setup may take 1–2 hours. After that, monthly reviews are much faster and easier to maintain.

Learn More on SmartMoneyTrek

Explore our core financial guides:

- Save Money – proven ways to cut bills and build savings

- Budgeting – Tools and strategies to control your money

- Make Money – real side hustles and income ideas

- Loans & Debt – How to borrow wisely and eliminate debt

The Long-Term Impact of Zero-Based Budgeting

Over time, zero-based budgeting does more than balance your monthly numbers — it reshapes your financial behavior.

It builds:

- Greater financial confidence

- Reduced money-related stress

- Clearer spending priorities

- Faster wealth accumulation

- Stronger, more disciplined decision-making

As consistency compounds, your relationship with money changes. You stop reacting to expenses as they arise. You start directing your income with clarity and purpose.

Final Thoughts: Becoming the CEO of Your Money

Zero-based budgeting isn’t just a method — it’s intentional financial leadership.

When you assign every dollar a purpose:

- Spending aligns with your goals.

- Saving becomes consistent and automatic.

- Debt declines with focused effort.

- Financial stress decreases.

You no longer wonder where your money went. You decide where it goes.

That shift — from passive observer to active architect — is where real financial transformation begins.

Start simple. Be patient during the first few months. Adjust, improve, and refine as you go. With time, managing your money this way will feel natural — and far more powerful than the alternative.

This content is for educational purposes only and does not constitute financial advice.