How to Budget With Irregular Income (Freelancers & Self-Employed): A Complete Guide

📘 In This Guide 👇

- Introduction to budgeting with irregular income

- Key Takeaways

- What Is Budgeting With Irregular Income?

- Why Budgeting for Freelancers Is Becoming Essential

- Understanding the Financial Reality of Irregular Income

- The 4-Account Freelance Budget System

- Shift Your Financial Thinking: From Monthly to Strategic Planning

- Step 1: Identify Your Essential Living Expenses

- Step 2: Determine Your Average Monthly Income

- Step 3: Separate Personal and Business Finances

- Step 4: Pay Yourself a Consistent Monthly Salary

- Step 5: Build a Financial Buffer (The Stability Reservoir)

- Step 6: Create a One-Month Financial Buffer

- Step 7: Use Percentage-Based Budgeting

- Step 8: Plan for Taxes Before They Become a Problem

- Step 9: Prepare for the “Feast and Famine” Cycle

- Step 10: Build a Strong Emergency Fund

- Step 11: Stabilize Your Income Sources

- Step 12: Track Your Finances Regularly

- Step 13: Avoid Lifestyle Inflation

- Step 14: Invest for Long-Term Financial Growth

- Common Budgeting Mistakes Freelancers Make

- Frequently Asked Questions

- Final Thoughts: Turning Income Uncertainty Into Financial Freedom

Introduction to budgeting with irregular income

Freelancing and self-employment represent one of the most significant shifts in the modern economy. Professionals across industries—consultants, creators, developers, writers, designers, and independent contractors—are increasingly choosing flexible career paths that prioritize autonomy and opportunity over the traditional structure of fixed salaries. While this freedom can unlock remarkable earning potential, it also introduces a central financial challenge: how to budget with irregular income.

Unlike employees who receive predictable paychecks, freelancers operate within a dynamic financial environment where income can vary from month to month. One period may bring multiple well-paid projects, while another may involve delayed payments or slower client activity. This pattern—commonly referred to as the “feast and famine cycle”—makes irregular income budgeting far more complex than conventional personal finance advice suggests.

Yet financial stability is not reserved only for those with steady salaries. In fact, many independent professionals build strong financial systems by mastering budgeting for freelancers, adopting disciplined freelance money management, and developing intentional freelance financial planning strategies designed specifically for variable earnings.

The key lies in shifting away from traditional budgeting models that assume consistent income. Instead, freelancers and independent workers must learn the art of managing variable income—creating flexible financial structures that can adapt to both high-earning months and slower seasons without disrupting long-term stability.

This guide explores practical and proven principles for budgeting for self-employed professionals. By implementing a strategic approach to saving, spending, and planning around income fluctuations, freelancers can build financial resilience, reduce uncertainty, and transform unpredictable earnings into a stable and sustainable financial life.

For a more comprehensive approach to budgeting, refer to our complete monthly budgeting guide, which provides a structured framework for building and managing an effective monthly budget.

Key Takeaways

- Freelancers must build financial buffers because income fluctuates.

- Use average income rather than last month’s income for budgeting.

- Separate business income, taxes, and personal salary accounts.

- Pay yourself a consistent salary to stabilize cash flow.

- Build 6–12 months of emergency savings to survive slow months.

This guide is based on proven budgeting systems used by financial counselors, nonprofit credit agencies, and long-term savers around the world.

At SmartMoneyTrek, we focus on practical personal finance systems designed for real people — especially those building stability from limited income.

What Is Budgeting With Irregular Income?

Budgeting with irregular income is a financial strategy that helps freelancers, entrepreneurs, and self-employed professionals manage money even when earnings fluctuate each month.

The key principles include:

- Calculating essential monthly expenses

- Using average income to plan spending

- Paying yourself a fixed monthly salary

- Building a financial buffer for slow months

- Saving a portion of every payment for taxes

This approach focuses on cash-flow stability rather than fixed monthly income, allowing freelancers to stay financially secure despite income variability.

Why Budgeting for Freelancers Is Becoming Essential

The freelance economy has expanded rapidly in recent years, with millions of professionals now relying on independent work as their primary source of income.

- Greater workforce participation as more professionals choose freelancing for flexibility and autonomy.

- Irregular income patterns caused by project-based or seasonal work.

- Increased need for financial structure to manage income volatility and maintain financial stability.

Understanding the Financial Reality of Irregular Income

Traditional budgeting methods are built around a simple assumption: income arrives consistently. When a fixed paycheck is received on a predictable schedule, it becomes straightforward to allocate money toward living expenses, savings, and long-term investments.

Freelancers and self-employed professionals operate in a different financial environment.

Income can fluctuate significantly due to project-based work cycles, delayed client payments, seasonal demand, changing market conditions, or different stages of business growth. These realities mean that budgeting for irregular income cannot rely on fixed monthly expectations. Instead, it must focus on effective cash-flow management.

Rather than asking, “How do I budget this month’s paycheck?” independent professionals must approach freelance financial planning with a broader question: “How do I build a financial system that remains stable during both high-income and low-income months?”

Sustainable **freelance money management** begins with this crucial mindset shift—designing a flexible budgeting framework that adapts to income variability while maintaining financial stability.

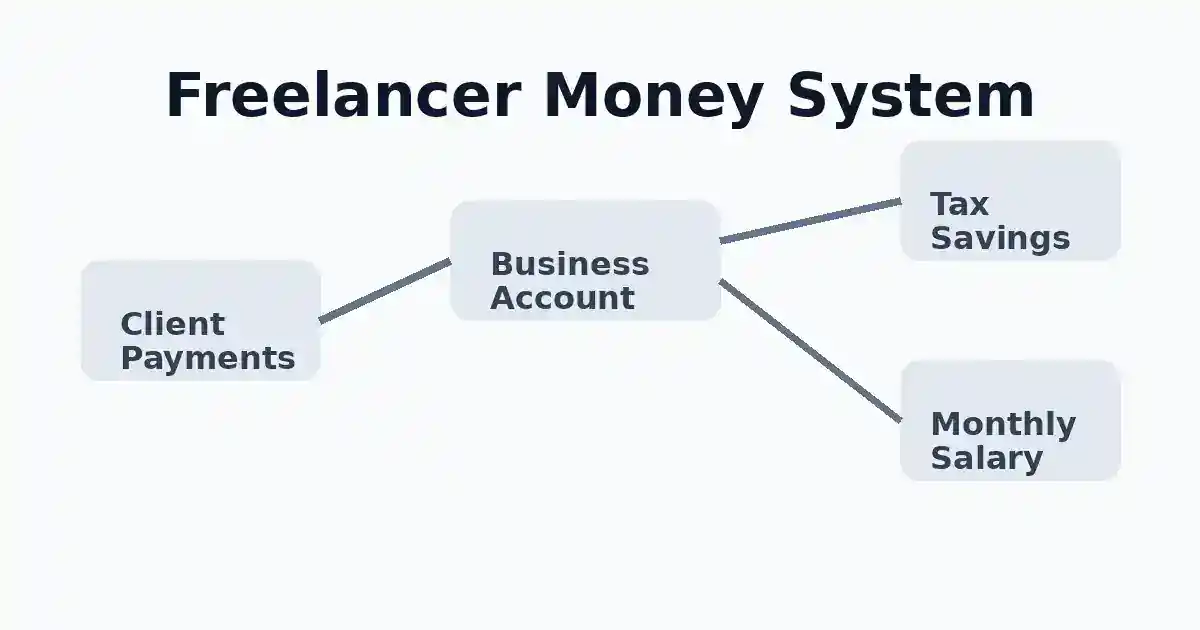

The 4-Account Freelance Budget System

Freelancers can manage irregular income more effectively by using a simple four-account budgeting system:

- Business income account – receives all client payments.

- Tax savings account – sets aside money for taxes.

- Personal salary account – transfers a consistent income for living expenses.

- Emergency reserve account – builds a buffer for slow months or unexpected costs.

Separating money into dedicated accounts clarifies financial responsibilities and makes budgeting easier to manage.

Saving money works best when you are tracking every dollar with a monthly budget.

Shift From Monthly Thinking to Strategic Financial Planning

One of the most common financial mistakes freelancers make is planning their spending around the most recent payment received. A large project payment can create a false sense of financial abundance, often leading to unnecessary spending. Conversely, a slow month may trigger anxiety and financial pressure.

This reactive cycle weakens both financial stability and professional focus. A more effective approach is to adopt strategic financial planning by clearly separating business income from personal spending.

Think of your freelance career as a business—“You, Inc.” Your freelance work generates revenue, and you are also the employee who receives compensation from that business. The objective is to create a system where the employee (you) receives stable, predictable income, even when the business experiences revenue fluctuations.

This simple but powerful mindset shift turns unpredictable earnings into structured and controlled cash flow.

If you don’t yet have a simple tracking system, follow our complete beginner budgeting guide to see where your money is leaking and how to plug those holes.

Step 1: Identify Your Essential Living Expenses

The foundation of budgeting with irregular income begins with a clear understanding of your minimum monthly financial needs. This represents the baseline amount required to maintain a stable and functional lifestyle.

Essential expenses typically include:

- Housing (rent or mortgage)

- Groceries and basic food needs

- Utilities and electricity

- Transportation

- Phone and internet services

- Insurance

- Minimum debt repayments

- Basic healthcare costs

If your income is currently limited, consider increasing it with realistic side income ideas for beginners.

When these expenses are combined, they form your minimum survival budget—the lowest monthly income required to sustain financial stability.

For freelancers and self-employed professionals, this number is extremely valuable. Knowing your baseline financial requirement removes uncertainty and provides a clear target for managing variable income. Instead of guessing how much you need to earn, you operate with a defined threshold that supports confident and disciplined freelance money management.

Step 2: Determine Your Average Monthly Income

Because freelance earnings fluctuate, the most reliable way to estimate your financial capacity is by calculating your average monthly income. This provides a realistic foundation for managing variable income and maintaining stability.

Review your income from the past 6–12 months, then calculate the average.

| Month | Income |

|---|---|

| January | $2,500 |

| February | $1,800 |

| March | $3,200 |

| April | $2,000 |

| May | $2,700 |

| June | $1,600 |

| Total | $13,800 |

| Average Monthly Income | $2,300 |

However, effective irregular income budgeting requires a conservative approach. Instead of planning your budget around your highest-earning months, base it on your lower-income periods.

This strategy creates a financial cushion, ensuring your budget remains sustainable even during slower seasons of freelance financial planning.

If you’re starting from zero, read our step-by-step emergency fund guide to build financial security faster.

Step 3: Separate Personal and Business Finances

A common mistake in freelance money management is mixing personal and business funds. When all income and expenses pass through a single account, it becomes difficult to track business performance, control spending, or prepare accurately for taxes.

A more disciplined approach is to create a clear financial structure using separate accounts:

1. Business Income Account

All client payments and project earnings are deposited here first. This account represents the revenue of your freelance business.

2. Tax Savings Account

A predetermined percentage of every payment is transferred here to cover future tax obligations.

3. Personal Salary Account

From the business income, you transfer a consistent monthly amount to this account for personal living expenses.

This system treats your freelance work like a business and ensures you pay yourself a predictable income. The result is greater financial clarity, improved irregular income budgeting, and stronger long-term financial control.

For those who prefer more precision and control, zero-based budgeting assigns every dollar a specific purpose.

High monthly bills often lead to debt. If that’s your situation, visit our how to reduce debt and stop high interest payments eating your income.

Step 4: Pay Yourself a Consistent Monthly Salary

A common challenge in freelance financial planning is the tendency to spend money immediately after client payments arrive. While this may feel natural, it often leads to unstable finances and inconsistent spending patterns. A more effective approach is to pay yourself a fixed monthly salary.

Here’s how the system works:

- All client payments are deposited into your business income account.

- You determine a stable monthly salary based on your conservative income estimate.

- At the beginning of each month, you transfer that amount to your personal account for living expenses.

Example:

- Average monthly income: $2,300

- Chosen personal salary: $1,800

The remaining funds stay in the business account to build a financial buffer for slower months. This approach stabilizes your personal finances and smooths the natural peaks and valleys that come with managing variable income.

If your income is tight, learn learn realistic ways to increase your income with proven side hustles so you can improve your savings rate.Step 5: Build a Financial Buffer (The Stability Reservoir)

A critical component of budgeting with irregular income is creating a financial buffer—a dedicated reserve that protects you during low-income periods. This buffer functions as a stability reservoir, absorbing the natural fluctuations that come with freelance earnings. Instead of allowing slow months to disrupt your finances, the reserve ensures continuity.

Ideally, freelancers should aim to accumulate three to six months of their personal salary in this fund.

- When income exceeds expectations, surplus earnings strengthen the reservoir.

- During slower periods, the buffer supports your regular salary without financial pressure.

Over time, this strategy transforms irregular income budgeting from a stressful guessing game into a structured system, allowing freelancers to maintain stability and confidence regardless of income cycles.

Step 6: Create a One-Month Financial Buffer

Another powerful strategy in irregular income budgeting is the one-month buffer rule—living on the previous month’s income instead of relying on current earnings. Under this system, the income you earn today is used to fund the following month’s expenses.

Example:

- March income covers April expenses

- April income covers May expenses

This structure creates valuable financial breathing room. Instead of depending on incoming payments to meet immediate bills, you operate with a full month of financial distance between earning and spending.

For freelancers and self-employed professionals, even a single buffer month can significantly reduce financial pressure and improve long-term freelance money management.

Learn More on SmartMoneyTrek

Explore our core financial guides:

- Save Money – proven ways to cut bills and build savings

- Budgeting – Tools and strategies to control your money

- Make Money – real side hustles and income ideas

- Loans & Debt – How to borrow wisely and eliminate debt

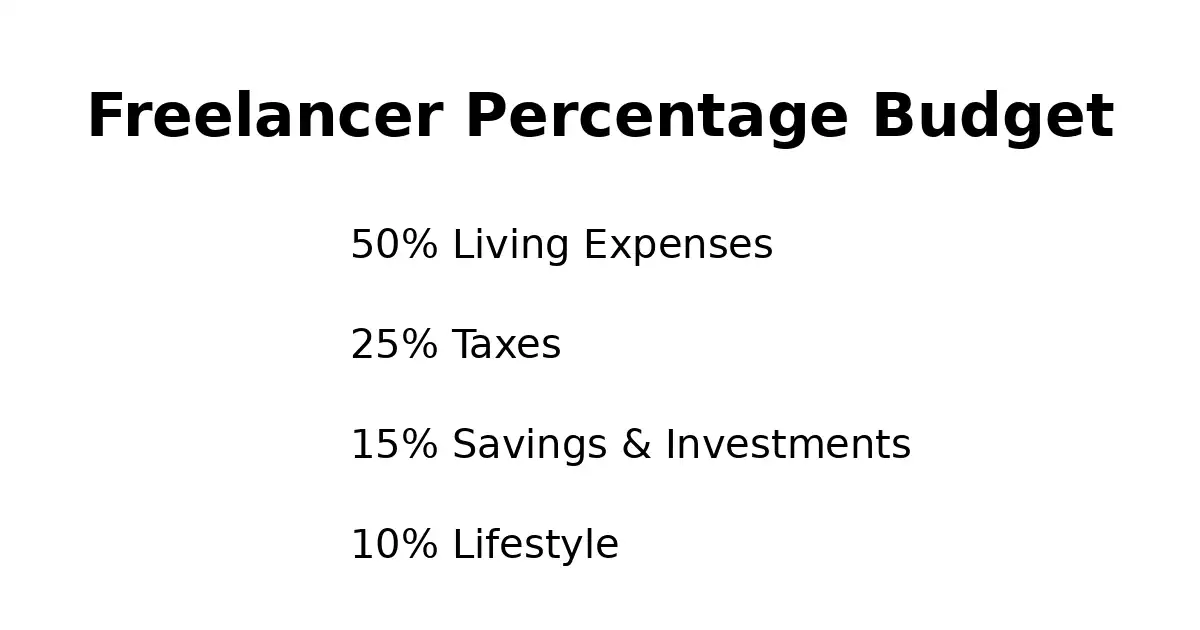

Step 7: Use Percentage-Based Budgeting

When income fluctuates, maintaining fixed spending amounts can become difficult. A more adaptable approach for budgeting for freelancers is percentage-based budgeting, where income is allocated according to proportions rather than fixed figures. This structure allows your financial plan to adjust naturally as income changes, supporting effective managing of variable income.| Category | Recommended Percentage |

|---|---|

| Living Expenses | 50% |

| Taxes | 20–30% |

| Savings & Investments | 15–20% |

| Lifestyle Spending | 5–10% |

With this system, higher-income months automatically increase savings and financial reserves, while lower-income months naturally reduce discretionary spending—creating a flexible and sustainable framework for irregular income budgeting.

Step 8: Plan for Taxes Before They Become a Problem

Taxes can become a major financial shock for freelancers if they are not planned for early. Unlike traditional employees, freelancers do not have taxes automatically deducted from their income, making proactive freelance financial planning essential. A disciplined strategy is to set aside 20%–30% of every client payment immediately for taxes.

Example:

- Client payment: $1,000

- Tax reserve (25%): $250

- Available income: $750

Keeping this tax reserve in a separate account ensures the funds remain untouched and available when tax obligations arise. By treating taxes as a priority expense rather than an afterthought, freelancers can maintain stronger financial control and avoid unnecessary stress during tax season.

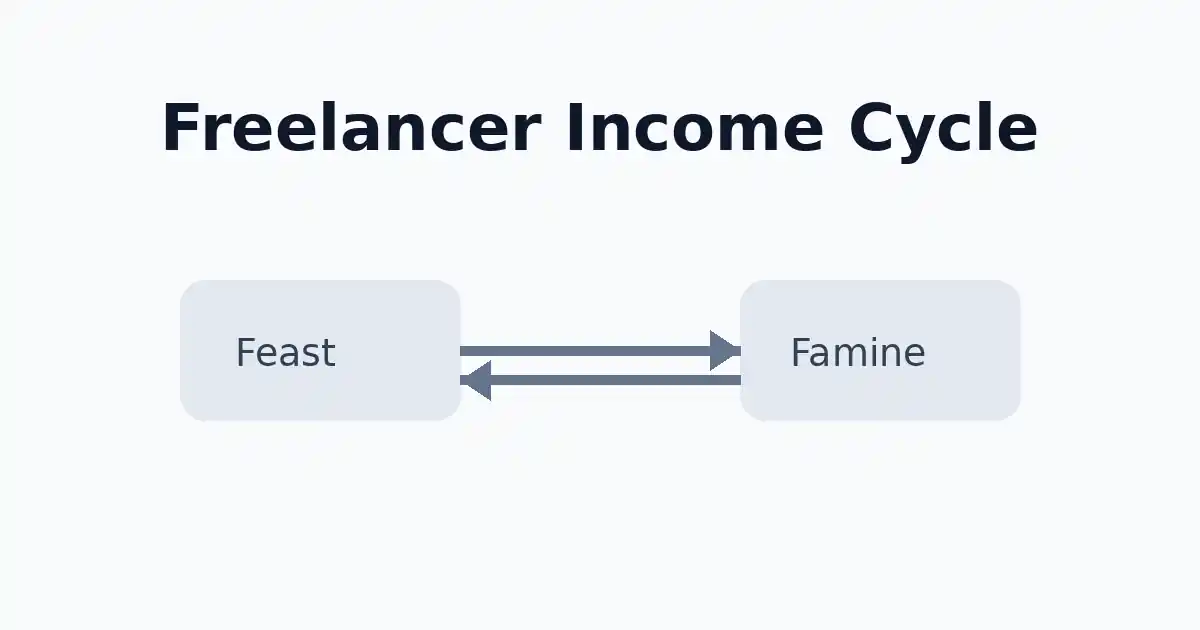

Step 9: Prepare for the “Feast and Famine” Cycle

Freelancers naturally experience two financial phases: high-income periods and slow earning periods. Understanding and preparing for this cycle is essential for sustainable irregular income budgeting.

Feast periods occur when multiple projects or clients generate higher-than-usual income. These months should be used strategically to strengthen your financial position by increasing savings, building emergency reserves, reducing debt, and investing in tools or skills that expand your earning capacity.

Famine periods, on the other hand, bring fewer projects or delayed payments. During these times, disciplined freelance money management becomes critical—reducing non-essential spending, relying responsibly on saved reserves, and focusing energy on client outreach, networking, and marketing.

Freelancers who plan intentionally for both phases transform income volatility into a manageable cycle, creating long-term financial stability rather than uncertainty.

Step 10: Build a Strong Emergency Fund

For freelancers and self-employed professionals, an emergency fund is not optional—it is a critical financial safeguard. Unlike traditional employees, freelancers do not have employer protections such as severance pay, paid leave, or stable salaries during disruptions.

While many financial experts recommend 3–6 months of expenses for salaried workers, freelancers benefit from a larger safety margin. A more resilient target is 6–12 months of essential living expenses.

This reserve protects you from unexpected challenges such as:

- Sudden health issues

- Losing major clients

- Economic slowdowns

- Business interruptions

By maintaining a strong emergency fund, freelancers create a financial safety net that preserves stability during uncertainty, making long-term freelance financial planning far more secure.

Not sure where to start? Our guide on how to build an emergency fund from scratch breaks it down step by step.

Step 11: Stabilize Your Income Sources

While effective budgeting is essential, income stability is equally important for long-term freelance success. Reducing dependence on a single income source helps protect against sudden financial disruptions.

Freelancers can strengthen income stability through several strategic approaches:

Diversify Clients

Avoid relying heavily on one client. A broader client base reduces the risk of sudden income loss.

Secure Retainer Contracts

Ongoing monthly retainers provide predictable revenue and improve financial consistency.

Offer Multiple Services

Expanding your skill set allows you to serve different market needs and reduces reliance on a single type of project.

Develop Passive Income Streams

Developing passive income streams can further strengthen financial stability. Digital products, affiliate marketing, and online courses can generate income beyond active client work.

If you're looking for practical ideas to diversify your earnings, explore our guide on the 20 best side hustles to start today.

By building multiple and reliable income streams, freelancers create stronger financial resilience and a more stable foundation for long-term freelance money management.

Step 12: Track Your Finances Regularly

Consistent financial tracking is essential for effective freelance money management. Because income and expenses can change quickly, freelancers benefit from frequent financial check-ins rather than occasional reviews.

A simple weekly review helps maintain control by answering key questions:

- What income was received this week?

- What expenses occurred?

- Am I staying on track with savings and financial goals?

Helpful tools for monitoring your finances include budget spreadsheets, accounting software, and personal finance apps.

Helpful tools for monitoring your finances include budget spreadsheets, accounting software, and personal finance apps. You can also use our SmartMoneyTrek Ultimate Budget Kit to track income, expenses, and savings more effectively.

Regular tracking strengthens financial awareness, allowing freelancers to identify trends early, adjust spending when necessary, and prevent small financial issues from growing into major problems.

Step 13: Avoid Lifestyle Inflation

High-income months can create the temptation to quickly upgrade your lifestyle. Freelancers may feel encouraged to move into more expensive housing, purchase luxury items, or add new recurring subscriptions.

However, irregular income requires financial restraint. Because high-earning periods may not be consistent, expanding fixed expenses too quickly can create financial pressure during slower months.

A more disciplined strategy is to prioritize saving and financial reserves before increasing lifestyle spending. Strengthening your savings, investments, and financial buffers first ensures that temporary income spikes translate into long-term financial security rather than short-term consumption.

This approach helps freelancers maintain stability and protect their finances despite income fluctuations.

Step 14: Invest for Long-Term Financial Growth

Effective budgeting is not only about controlling expenses—it is also about building long-term wealth. For freelancers and self-employed professionals, intentional investing is essential for financial independence and future security.

Key investment avenues to consider include:

- Retirement accounts

- Stock market investments

- Index funds

- Real estate opportunities

- Reinvesting in your business

Consistent contributions, even in modest amounts, can grow substantially over time through compound growth. The earlier you begin investing, the greater the long-term impact on your financial future.

By integrating investing into your freelance financial planning, you transform budgeting from simple money management into a strategy for sustainable wealth creation.

Common Budgeting Mistakes Freelancers Make

- Spending income immediately instead of allocating funds for essential obligations first.

- Not setting aside money for taxes, which can create financial stress when payments are due.

- Depending on a single major client, increasing income risk if that client leaves.

- Raising lifestyle expenses during high-income months, making slow months harder to manage.

- Failing to build a financial buffer to cover periods of low or inconsistent income.

Frequently Asked Questions

Budgeting with irregular income involves identifying essential monthly expenses, estimating your average earnings, and paying yourself a consistent salary from your business income. Freelancers also benefit from building a financial buffer and saving part of every payment for taxes.

Percentage-based budgeting works well for freelancers because it adjusts automatically when income rises or falls. Many freelancers allocate portions of income to living expenses, taxes, savings, and lifestyle spending.

Freelancers are usually advised to save six to twelve months of essential expenses. Because income can fluctuate, a larger emergency fund provides security during slow business periods or unexpected financial challenges.

Yes. Keeping business and personal finances separate improves financial organization, simplifies budgeting, and makes it easier to prepare taxes. Many freelancers use separate accounts for business income, tax savings, and personal salary.

Freelancers often work on project-based contracts, which means income can vary each month. Some months bring multiple projects and higher income, while other months may have fewer clients or delayed payments.

A common recommendation is to set aside between 20% and 30% of every payment for taxes. Keeping this money in a separate account helps ensure it is available when tax payments are due.

The safest budgeting rule for freelancers is to base spending on your lowest expected monthly income rather than your highest earnings. This conservative approach ensures essential expenses remain covered even during slow months.

Yes. Freelancers can adapt the 50/30/20 budgeting rule by allocating about 50% of income to essential expenses, 30% to lifestyle spending, and 20% to savings or debt repayment. However, many freelancers modify this rule to save more during high-income months.

Freelancers survive slow months by building financial buffers during high-income periods. Maintaining emergency savings, paying themselves a fixed monthly salary, and diversifying income sources helps stabilize finances when work temporarily slows down.

Yes. Separate savings accounts help freelancers organize finances more effectively. Many freelancers maintain individual accounts for taxes, emergency savings, and business reserves to ensure money is allocated for its intended purpose.

Final Thoughts: Turning Income Uncertainty Into Financial Freedom

Budgeting with irregular income requires a different mindset from traditional financial planning. Freelancers and self-employed professionals must rely on systems built around flexibility, discipline, and long-term strategy rather than predictable paychecks.

By identifying essential expenses, calculating a realistic income average, paying yourself a consistent salary, saving aggressively during high-income periods, and maintaining strong financial buffers, it is possible to create stability even when income fluctuates.

Ultimately, financial success as a freelancer is not defined by the income earned during your best month. It is determined by how effectively you manage money across both strong and slow periods.

With thoughtful irregular income budgeting and disciplined freelance money management, income volatility can shift from a source of uncertainty into a foundation for long-term independence, stability, and financial freedom.

Ready to Apply This Budgeting Method?

Learn how to create a simple monthly budget step by step and start organizing your income today. Create Your Monthly Budget

Your financial journey doesn’t need to begin with perfection. It simply needs to begin with consistency — because consistent action, over time, is what turns small steps into lasting progress.

This content is for educational purposes only and does not constitute financial advice.